Take control of your financial future with these 15 smart financial planning ideas designed specifically for single women.

From building an emergency fund and investing early to planning retirement and creating multiple income streams, this guide covers everything you need to achieve financial independence.

Learn how to budget effectively, avoid high-interest debt, protect yourself with insurance, and grow your income confidently.

Whether you’re just starting your career or looking to strengthen your financial foundation, these practical tips will help you build security, stability, and long-term wealth on your own terms.

Start making empowered money decisions today.

1. Build a 6-Month Emergency Fund

An emergency fund is your financial safety cushion.

Life is unpredictable — job loss, medical emergencies, family responsibilities, or sudden expenses can arise anytime.

Aim to save at least six months’ worth of essential expenses (rent, groceries, EMIs, utilities).

Keep this money in a separate savings account or liquid fund so it’s easily accessible. Having this fund reduces stress and prevents you from relying on credit cards or loans during tough times.

2. Get Health Insurance Early

Medical expenses are increasing every year.

Even if you are young and healthy, health insurance is essential. Buying a policy early ensures lower premiums and better coverage.

Relying only on employer-provided insurance can be risky because it may not cover you if you switch jobs.

A personal health insurance policy gives you long-term protection and financial security.

3. Start Investing Early (Even with Small Amounts)

You don’t need a large salary to begin investing. Starting early is more important than starting big.

Even small monthly investments through SIPs, index funds, or recurring deposits can grow significantly over time due to compounding.

The earlier you start, the less pressure you’ll feel later. Investing is how you make your money work for you.

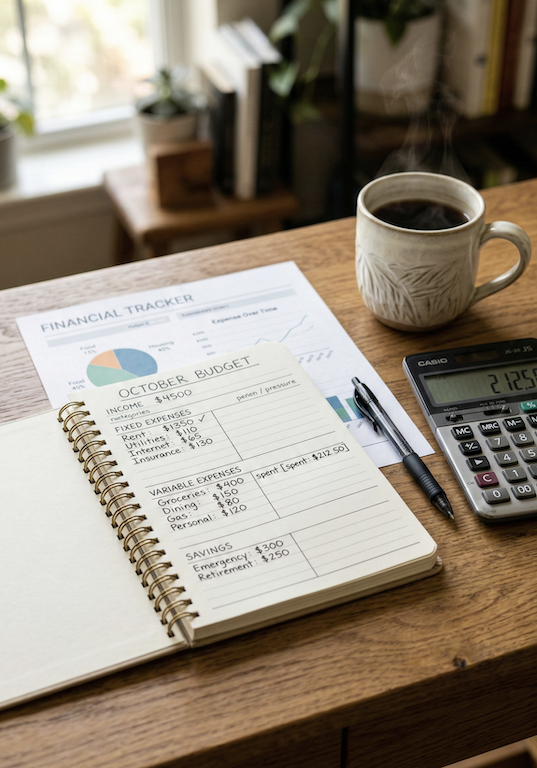

4. Create a Monthly Budget You Can Actually Follow

A realistic budget helps you understand where your money is going.

Divide your income into essentials, lifestyle expenses, and savings.

The 50/30/20 rule is a simple framework: 50% needs, 30% wants, 20% savings.

Tracking your expenses regularly helps you control unnecessary spending and stay aligned with your financial goals.

5. Increase Income, Not Just Savings

While saving is important, increasing your income can accelerate financial growth.

Consider upgrading your skills, negotiating your salary, freelancing, or starting a side hustle. When income grows, your ability to invest and build wealth increases.

Focus on earning more, not just cutting expenses.

6. Plan for Retirement Now

Many women delay retirement planning, thinking it’s too early.

But women generally live longer than men, which means you’ll need a larger retirement corpus. Starting early gives your investments more time to grow.

Contributing to pension schemes, retirement funds, or long-term investments ensures financial independence in later years.

7. Avoid Lifestyle Inflation

When your income increases, it’s tempting to upgrade your lifestyle immediately.

However, increasing expenses at the same rate as income prevents wealth building.

Instead, maintain your current lifestyle and invest the extra income.

This habit significantly improves long-term financial stability.

8. Create Multiple Income Streams

Depending on a single salary can be risky.

Building multiple income sources — such as freelancing, digital products, rental income, or investments — provides financial security.

If one income stream slows down, others can support you. Diversified income creates stability and faster wealth growth.

9. Learn Basic Tax Planning

Understanding taxes helps you save money legally.

Learn about tax-saving investments, deductions, and exemptions available to you.

Smart tax planning reduces your liability and increases your take-home income.

Instead of paying unnecessary taxes, redirect that money toward investments.

10. Protect Yourself with Term Insurance

If you have dependent parents, siblings, or loans, term insurance is essential.

It ensures that your financial responsibilities are covered even in your absence. Term insurance is affordable and provides high coverage.

It’s a simple yet powerful way to protect your loved ones.

11. Keep Your Finances Organized

Maintain clear records of your investments, insurance policies, bank accounts, and nominee details.

Keep digital and physical copies of important documents.

Financial organization prevents confusion and ensures your family can access information when needed.

Clarity reduces stress and improves decision-making.

12. Avoid High-Interest Debt

Credit card debt and personal loans often come with high interest rates. If not managed properly, they can quickly become overwhelming.

Always try to pay your credit card balance in full each month.

Avoid borrowing for lifestyle purchases. Debt should be used strategically, not emotionally.

13. Invest in Skill Development

Your skills are your biggest asset. Investing in courses, certifications, or learning new technologies increases your earning potential. T

he more valuable your skills, the more opportunities you create for yourself.

Personal growth directly impacts financial growth.

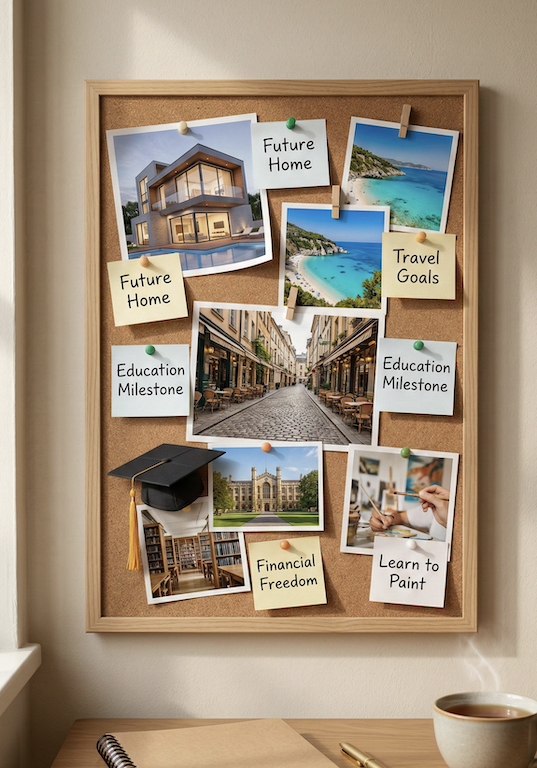

14. Plan Big Life Goals Independently

Whether it’s buying a house, traveling, pursuing higher education, or starting a business — plan your goals independently.

Don’t assume someone else will finance your dreams.

Create goal-based investment plans and calculate how much you need to save monthly to achieve them.

15. Build Financial Confidence

Money management is a skill, not a talent you’re born with.

The more you learn about finance, the more confident you become. Read books, follow financial experts, and educate yourself regularly.

Financial confidence empowers you to make bold decisions and live life on your own terms.